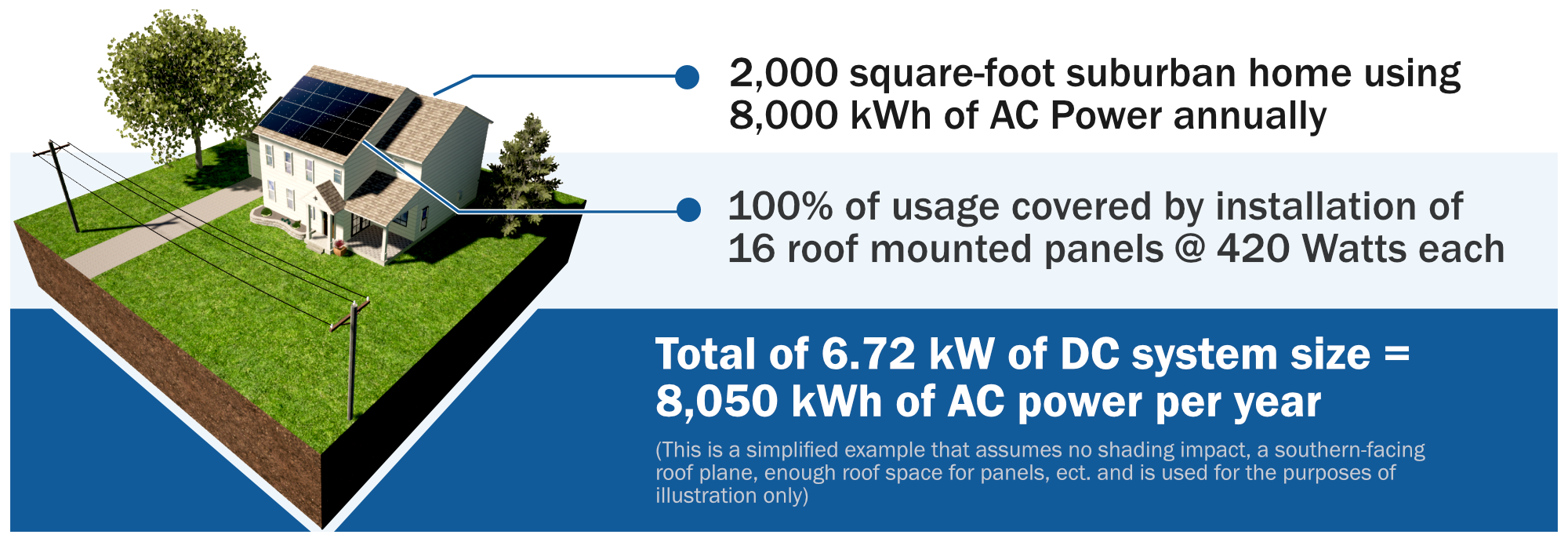

There are a variety of ways to reduce the out-of-pocket contribution and finance the cash required. Below we explain available NY solar incentives and financing options, and apply each to a real-life example:

By taking advantage of government incentives and tax credits, a solar power plant for your home is a solid financial investment. Payback periods are short, return on investment high, and you fix your energy costs well into the future. There are three levels to these as follows:

1

NY-SUN Solar PV Rebate or Incentive ($0.15/W)

Based on DC system size and performance of the array. As good as cash directly off the project cost.

2

Federal Tax Credit (30%)

Direct bottom-line deduction from federal tax bill.

3

NYS Tax Credit (25% up to $5,000)

Direct bottom-line deduction from state tax bill.

Example: Solar Credits & Incentives

Here’s how the federal and NY solar incentives and tax credits play out using the example above:

System Cost

$21,250

NY-SUN Solar PV Rebate ($0.15/W) Like cash off; goes directly to system builder upon completion.

-$1,008

Contract Cost

$20,242

30% Federal Tax Credit Based on contract cost ($20,242 x .30); deduction from federal tax bill for year paid

-$6,072

25% NYS tax credit ($5,000 maximum) Based on contract cost ($20,242 x .25); deduction from state tax bill for year paid

Installing a solar array is a smart investment—but it must make sense financially for your family. It’s possible to lease a system with no money down, but it’s not advised. These financing options are far more advantageous:

1

Home Equity Line of Credit (6.42% – 8.95%)

Secured loan typically provides the lowest interest rates. Can cover full contract cost, including state and federal taxes for zero money out of pocket

2

NYSERDA Smart Energy Loan (Currently 4.00% or 7.50%)

15 year loan that can cover up to $25,000 of total system cost. Two loan rates offered depending on location and income.

3

Credit Human Solar System Loans (7.99%)

10, 15 or 20 year loans that can cover entire contract cost (up to $100,000). Once received, tax credits can be used to re amortize loan at no cost for lower monthly payments, or kept for other use.

Example: Financing Options

Here’s how these options break down using the example above: